EDUCATIONAL RESOURCES

Market Update

Market Navigator for the Month Ending July 31, 2026

Presented by John B. Steiger, AIFA®, CFP®

The lack of progress in negotiations to end the war in the Middle East and a return to military action led to a 21 percent rise in oil prices and a mixed month for stocks. Much of the weakness was concentrated in several high-flying artificial intelligence beneficiaries focused on semiconductors and memory. However, underlying trends in the market remained positive.

1. Beyond the Headlines: Volatility Masks Improving Underlying Trends

2. Fixed Income Update: A Volatile Month

3. Geopolitical and Economic Update: Solid Fundamentals Despite Geopolitical Risks

4. Looking Ahead: Risks Exist but Fundamentals Should Provide Support for Markets

Beyond the Headlines: Volatility Masks Improving Underlying Trends

Given the sell-off in several growth areas of the market, the tech-heavy Nasdaq emerged as the worst performing major U.S. index in July. The small-cap Russell 2000 also was down. The S&P 500 and Dow Jones Industrial Average, however, were basically flat for the month. The equal-weighted S&P 500, which removes the size of the company from index weighting, once again outperformed the market-cap weighted version by more than 1 percent. This result indicated that while stocks in general were up, a few of the largest companies dragged the index lower. So despite volatility at the index level, there was also underlying strength, a good sign for investors.

We are now more than halfway through second-quarter earnings season and corporate America continued to exceed analysts’ expectations. Headline growth rates were impacted by some non-operating gains from some of the biggest names, but even if those are excluded, earnings growth would approach 29 percent. This figure compares to the 22 percent earnings growth analysts were expecting at the end of June. This would be the second-straight quarter of 20 percent-plus earnings growth for the S&P 500. In another encouraging sign, earnings estimates for both the third quarter and the full year moved higher in July. Continued growth in earnings should provide a solid backdrop for investors over the long term.

Fixed Income Update: A Volatile Month

Long-term Treasury yields came under pressure as oil prices rose, raising concerns about inflation, and the Federal Reserve continued to talk about addressing those concerns potentially through higher interest rates. As a result, negative returns occurred for most major U.S. bonds indices.

Concerns about the future path of inflation and whether the Fed will raise rates to address it played out in the Treasury market. Longer-term Treasury yields moved higher. The yield on the 30-year U.S. Treasury climbed above 5.2 percent, the highest level seen since 2007.

Geopolitical and Economic Update: Solid Fundamentals Despite Geopolitical Risks

Data was mixed but continued to point to economic growth over the remainder of the year. June jobs data came in below expectations after several consecutive months of higher jobs creation. The good news is that jobs growth was still positive, albeit at only 57,000 jobs created.

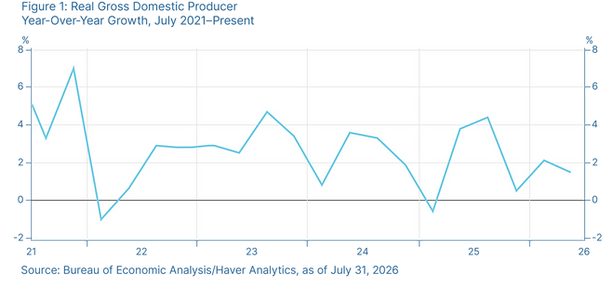

Second-quarter gross domestic product growth also came in below expectations at an annualized rate of 1.5 percent. This too was a slowdown from the first quarter’s 2.1 percent growth level. However, underlying trends in consumer spending and non-residential fixed investments were strong. Strength in these areas is an encouraging sign that the economy will continue to grow in the second half of the year.

Figure 1: Real Gross Domestic Producer Year-Over-Year Growth, July 2021–Present

Source: Bureau of Economic Analysis/Haver Analytics, as of July 31, 2026

At the end of July, the Fed met and announced it was holding interest rates steady. Although this was in line with market expectations, the possibility that the committee would raise rates was not out of the question. Fed Chair Kevin Warsh emphasized that the central bank remains committed to restoring price stability and repeatedly stressed that the Fed’s inflation target remains 2 percent. He also noted the committee would not hesitate to act if inflation remains stubbornly high. The next several reports on the labor market and consumer and producer inflation will play an important role in whether the Fed remains on hold or considers another rate increase later this year.

The Takeaway

-

Headline economic data remains mixed, but underlying trends indicate further growth ahead.

-

The Fed continues to focus on inflation, and a rate increase later in the year can’t be ruled out.

Looking Ahead: Risks Exist but Fundamentals Should Provide Support for Markets

The uncertainty surrounding inflation and how the Fed will react to it likely means continued volatility in both stocks and bonds as markets attempt to gauge its next steps. There are other risks as well that investors should monitor, led by the situation in the Middle East. Until a deal is announced that fully reopens the Strait of Hormuz, higher oil prices will continue to weigh on markets. Also, as attention begins to turn to the fall, midterm elections could cause increased volatility leading up to Election Day.

Macro data points remain solid for now, which should lead to continued economic growth, strong earnings growth from corporate America, and further market appreciation over the long term. We continue to believe that broadly invested portfolios remain the best way to participate in market upside while navigating ongoing uncertainty. If concerns remain, however, speak to your financial advisor to go over your financial plans.

Disclosure: This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.

Certain sections of this commentary contain forward-looking statements based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets. All indices are unmanaged and investors cannot invest directly into an index. The Dow Jones Industrial Average is a price-weighted average of 30 actively traded blue-chip stocks. The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. It excludes closed markets and those shares in otherwise free markets that are not purchasable by foreigners. The Bloomberg Aggregate Bond Index is an unmanaged market value-weighted index representing securities that are SEC-registered, taxable, and dollar-denominated. It covers the U.S. investment-grade fixed-rate bond market, with index components for a combination of the Bloomberg government and corporate securities, mortgage-backed pass-through securities, and asset-backed securities. The Bloomberg U.S. Corporate High Yield Index covers the USD-denominated, non-investment-grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below. One basis point (bp) is equal to 1/100th of 1 percent, or 0.01 percent. The Magnificent 7 (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia and Tesla) are a group of seven companies commonly recognized for their market dominance, their technological impact, and their changes to consumer behavior and economic trends.

Wealth Planning Resources is located at 303 Wyman Street, Suite 275, Waltham, MA and can be reached at 781.547.5620.

Securities and advisory services offered through LPL Financial, a registered investment advisor, member FINRA/SIPC

Authored by Chris Fasciano, chief market strategist, and Sam Millette, director, fixed income, at Commonwealth Financial Network®.

© 2026 Commonwealth Financial Network®